Insulation Market Size By Product (Glass Wool, EPS, XPS, Mineral Wool, CMS Fibre, Calcium Silicate, Aerogel, Cellulose, PIR, Phenolic Foam, and Polyurethane), By End-Use (Construction, Industrial, Transportation, HVAC & OEM, Appliances, Furniture/Bedding, and Packing), Regions, Segmentation, and Projection till 2029

CAGR: 7%Current Market Size: USD 58 BillionFastest Growing Region: Europe

Largest Market: APACProjection Time: 2022-2029Base Year: 2021

Global Insulation Market- Market Overview:

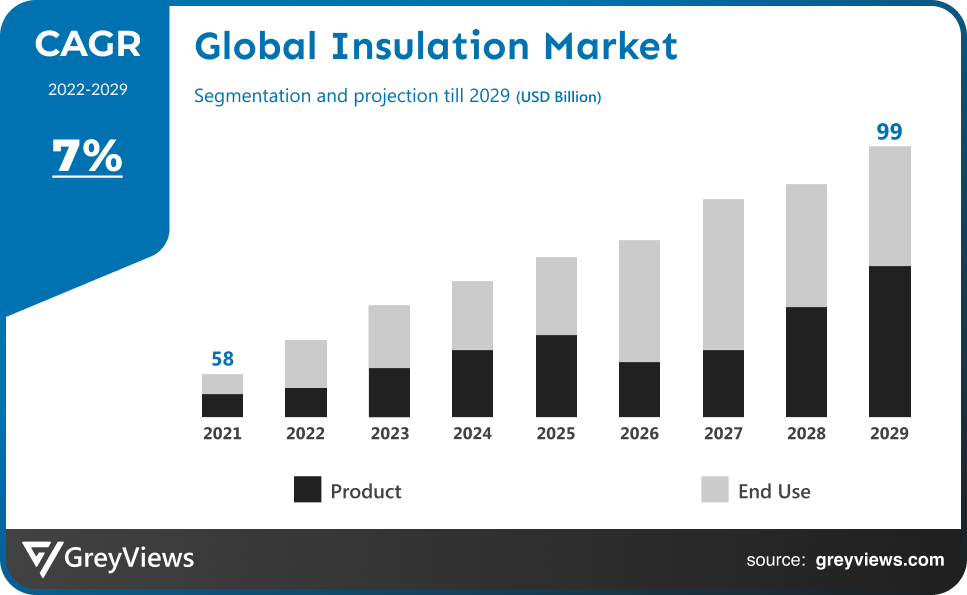

The global insulation market is expected to grow from USD 58 billion in 2021 to USD 99 billion by 2029, at a CAGR of 7% during the Projection period 2022-2029. The growth of this market is mainly driven owing to the increasing consumer awareness regarding energy conservation.

Insulation is a thin material that is mostly utilized in the textile and construction sectors. In the building and construction industries, insulation is frequently employed. The increase in global investments in energy-efficient infrastructure is the main factor driving the market growth. Urbanization and industrial growth are occurring at a rapid rate in both developing and developed economies, which has prompted governments and administrative bodies to significantly increase their spending on infrastructure development. Fiberglass and mineral wool are just two examples of the materials used in insulation. These materials are mostly utilized in homes to insulate air ducts. These goods are available in a variety of thicknesses. Over the course of the Projection period, rising consumer awareness of energy saving is anticipated to positively affect the market. Due to the COVID-19 crisis's economic slowdown, which was accompanied by poor investor confidence and a fall in building activity, the worldwide insulation market has only seen modest development. As a result, the market for insulation materials has also suffered a disastrous setback. The development of the engineering and building sectors was impacted by the COVID-19 pandemic in the United States. The pace of new and retrofit project sites in the residential and commercial sectors has been hindered by the stay-at-home directives and social distancing mandates.

Sample Request: - Global Insulation Market

Market Dynamics:

Drivers:

- Residential Sector is Rising

The market share of this particular category is growing as more attention is placed on lowering energy usage and the installation of effective, recyclable, and environmentally friendly materials. Rising consumer spending and the demand for new homes will both boost the insulation market's expansion. Product penetration will benefit from rising demand for insulating materials in residential and commercial applications in developed regions including North America and Europe. Market revenues will increase as a result of the building industry's expansion and an increase in energy-efficient technologies. Domestic players are anticipated to compete with multinational ones since greater client interaction is required. Strong distribution networks will likely be built by manufacturers in an effort to boost their profit margins. In addition, by reducing the heating and cooling loads in the building sector, the use of glass wool, plastic foam, and EPS can dramatically lower overall energy consumption.

Restraints:

- Environmental Concerns

Crude oil serves as the main raw source for the majority of insulating products. Since the bulk of the world's crude oil is produced by Middle Eastern nations, political unrest in these areas has a huge effect on crude oil supply and pricing globally. The equilibrium between supply and demand, which makes crude oil pricing extremely volatile, is another element that influences crude oil prices. The balance between the production and demand for crude oil has changed as a result of the economic slump in North America and Europe. It is anticipated that political upheaval in nations like Libya and Iraq may lower crude oil prices. The sanctioning of Russia's crude oil shipments is being postponed by the United States and Europe. The erratic price of crude oil directly affects the cost of raw materials.

Opportunities:

- Increase in the Government Policies

It is expected that new legislation and regulations will promote the use of contemporary construction methods. The expansion of the minimum needed thickness in building codes has aided in the adoption of these materials. The sector will grow as a result of rising population levels and a growing awareness of energy saving in developing countries. One of the main elements influencing the market penetration of insulation favorably is the adoption of zero-energy buildings and sustainable building practices. Fundamental features including high-performance structures, improved occupant comfort, noise reduction, and fire resistance are all made possible through insulation.

Challenges:

- Fluctuating Raw Material Prices

It is predicted that fluctuating raw material prices and rigorous environmental laws will impede market expansion in the years to come. According to estimates, the need for fiberglass insulation in industrial buildings would increase due to the significant presence of manufacturing businesses in China, India, Brazil, and Mexico. It's projected that this trend will accelerate market expansion even more. A current end-use trend predicted to spur industrial expansion is the rising demand for environmentally friendly homes as a result of population growth and fast urbanization.

Segmentation Analysis:

The global insulation market has been segmented based on product, end-use, and regions.

By Product

The product segment is glass wool, EPS, XPS, mineral wool, CMS fiber, calcium silicate, aerogel, cellulose, PIR, phenolic foam, and polyurethane. The glass wool segment led the largest share of the insulation market with a market share of around 12.76% in 2021. Over the Projection period, the glass wool product segment is anticipated to expand at a constant CAGR. Sand is the main component of glass wool, which provides insulating qualities for both sound and heat, including low weight and great tensile strength. Glass wool byproducts, such as removable blankets, are ideal for covering heat-generating uneven surfaces found on turbines, pumps, heat exchangers, tanks, expansion joints, valves, and flanges in industrial settings.

By End-Use

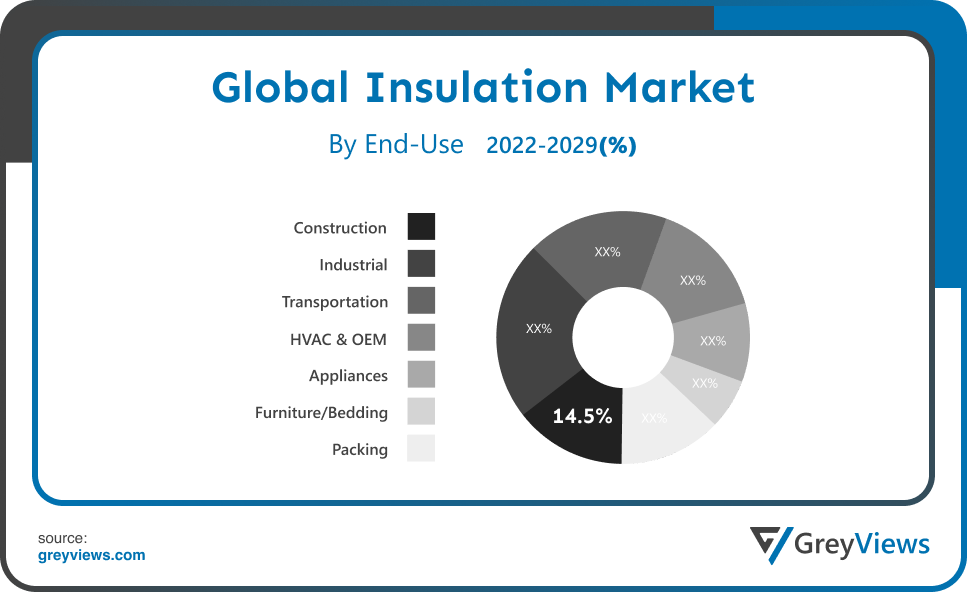

The end-use segment is construction, industrial, transportation, HVAC & OEM, appliances, Furniture/Bedding, and packing. The construction segment led the largest share of the insulation market with a market share of around 14.5% in 2021. Due to the rise in the number of buildings in metropolitan areas that require extensive insulation, the sector is anticipated to expand. The transportation and residential construction sectors, which are anticipated to develop at significant CAGRs from 2022 to 2030, came in second and third, respectively, behind the construction industry. For reasons including energy conservation, heat gain/loss reduction, temperature maintenance, efficient equipment operation or chemical reaction, condensation prevention, etc., the petrochemical industries and refineries are insulated.

Global Insulation Market- Sales Analysis.

The sale of insulation market products and end-use expanded at a CAGR of 5% from 2015 to 2021.

One of the major reasons fueling the market's expansion is the booming building sector. Along with the rapid growth in infrastructural development, particularly in emerging nations, there has been a noticeable increase in industrial and residential construction projects over time. Additionally, rising consumer awareness of energy conservation has a favorable effect on the market expansion. In order to meet the increased demand for power and energy caused by rapid urbanization and population growth, insulating materials are now being used extensively in a variety of construction projects. The industry is also expanding as a result of a considerable increase in the sales of cooling appliances like refrigerators and air conditioners. In order to reduce noise and vibrations and improve sound absorption, insulation materials are being employed more and more in automobiles.

Additionally, they support the production of several components including bumpers, roll pans, and wiper cowls. In the upcoming years, the market is also anticipated to be driven by additional factors such as technological developments in thermal insulation, increased disposable incomes, and various research and development (R&D) activities.

Thus, owing to the aforementioned factors, the global insulation market is expected to grow at a CAGR of 7% during the Projection period from 2022 to 2029.

By Regional Analysis:

The regions analyzed for the insulation market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. The Asia-Pacific region dominated the insulation market and held a 38% share of the market revenue in 2021.

- The Asia-Pacific region witnessed a major share. Due to worries over massive energy waste, rising oil output in China and India's economy, and the demand for materials for remodeling and refurbishing projects. The demand from high-temperature operational industries such as oil & gas, manufacturing, metal & mining, power, and others has a significant impact on the market. Additionally, businesses in this region are emphasizing loss reduction in order to enhance performance through the use of routine maintenance checks.

- Europe is anticipated to experience significant growth during the Projection period. Due to the fast industrialization and the existence of significant insulation product producers in Europe, the regional market is anticipated to be an early user of the developing insulation materials. The expansion of the downstream petrochemical sector and the increased product demand for the maintenance and repair of existing infrastructure are anticipated to be the primary drivers of market growth.

Global Insulation Market- Country Analysis:

- Germany

Germany's insulation market size was valued at USD 0.9 billion in 2021 and is expected to reach USD 1.32 billion by 2029, at a CAGR of 5% from 2022 to 2029.

It is anticipated that the local market would be an early user of developing insulation materials due to the region's increasing industrialization and the existence of significant insulation product producers in Germany. The purchase of vliepa GmbH (Germany), a business that specializes in coating, printing, and finishing nonwoven, paper, and film for the building materials market, was announced by Owens Corning in July 2021. With the acquisition, Owens Corning is now better equipped to support the European building and construction sector.

- China

China’s insulation market size was valued at USD 1.4 billion in 2021 and is expected to reach USD 2.3 billion by 2029, at a CAGR of 6.5% from 2022 to 2029. Because of china’s rising economy, worries about large energy waste, and the demand for materials in applications for rehabilitation and refurbishing. Additionally, companies in this area are concentrating on minimizing losses in order to improve performance by carrying out routine maintenance inspections.

- India

India's insulation market size was valued at USD 1.3 billion in 2021 and is expected to reach USD 2.07 billion by 2029, at a CAGR of 6% from 2022 to 2029. This is a result of the region's expanding population, quick industrialization, and growing demand for insulating goods in non-residential and residential construction.

Key Industry Players Analysis:

To increase their market position in the global insulation business, top companies focus on tactics such as adopting new technology, mergers & acquisitions, product developments, collaborations, partnerships, joint ventures, etc.

- GAF Materials Corp.

- Huntsman International LLC

- Johns Manville

- Cellofoam North America, Inc.

- Rockwool International A/S

- DuPont

- Owens Corning

- Atlas Roofing Corp.

- Saint-Gobain S.A.

- Kingspan Group

- BASF

- Knauf Insulation

Latest Development:

- In February 2020, Rockwool International AS purchased Parafon, a producer of stone wool-based acoustic solutions, with the intention of integrating it into its Rockfon subsidiary. Rockfon is expanding its customer base and market segments by acquiring this business in order to establish its footprint in northern Europe and capitalize on the capitalize acoustic performance of stone wool.

- In January 2020, Covestro AG and Recticel NV/SA joined up to make mattresses from old mattresses. This collaboration intends to create a circular economy in the polyurethane foam market, which is projected to help both businesses cut down on their use of raw materials.

Report Metrics

|

Report Attribute |

Details |

|

Study Period |

2021-2029 |

|

Base year |

2021 |

|

CAGR (%) |

7% |

|

Market Size |

58 billion in 2021 |

|

Projection period |

2022-2029 |

|

Projection unit |

Value (USD) |

|

Segments covered |

By Product, By End-Use And By Region. |

|

Report Scope |

Revenue Projection, competitive landscape, company ranking, growth factors, and trends |

|

Companies covered |

GAF Materials Corp., Huntsman International LLC, Johns Manville, Cellofoam North America, Inc., Rockwool International A/S, DuPont, Owens Corning, Atlas Roofing Corp., Saint-Gobain S.A., Kingspan Group, BASF, Knauf Insulation. |

|

By Product |

|

|

By End-Use |

|

|

Regional scope |

|

Scope of the Report

Global Insulation Market By Product:

- Glass Wool

- EPS

- XPS

- Mineral Wool

- CMS Fibre

- Calcium Silicate

- Aerogel

- Cellulose

- PIR

- Phenolic Foam

- Polyurethane

Global Insulation Market By End-Use:

- Construction

- Industrial

- Transportation

- HVAC & OEM

- Appliances

- Furniture/Bedding

- Packing

Global Insulation Market By Region:

- North America

- USA

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Russia

- Asia-Pacific

- Japan

- China

- India

- Korea

- Southeast Asia

- South America

- Brazil

- Peru

- Middle East and Africa

- UAE

- South Africa

- Saudi Arabia

Frequently Asked Questions

What will be the expected market size of the insulation market in 2029?

Global insulation market is expected to reach USD 99 billion by 2029, at a CAGR of 8% from 2022 to 2029.

What is the CAGR of the insulation market?

The insulation market is projected to have a CAGR of 7%.

What is the end-use segment of the insulation market?

On the basis of end-use, the amino acids market is segmented into construction, industrial, transportation, HVAC & OEM, appliances, Furniture/Bedding, and packing.

What are the key factors for the growth of the insulation market?

Due to increased demand for insulation in residential and non-residential applications, rising energy costs and the importance of energy conservation.

What is the breakup of the global insulation market based on the product?

Based on the product, the global insulation market has been segmented into glass wool, EPS, XPS, mineral wool, CMS fiber, calcium silicate, aerogel, cellulose, PIR, phenolic foam, and polyurethane.

Which are the leading market players active in the insulation market?

Leading market players active in the global insulation market are GAF Materials Corp., Huntsman International LLC, Johns Manville, Cellofoam North America, Inc., Rockwool International A/S, DuPont, Owens Corning, Atlas Roofing Corp., Saint-Gobain S.A., Kingspan Group, BASF, Knauf Insulation among others.

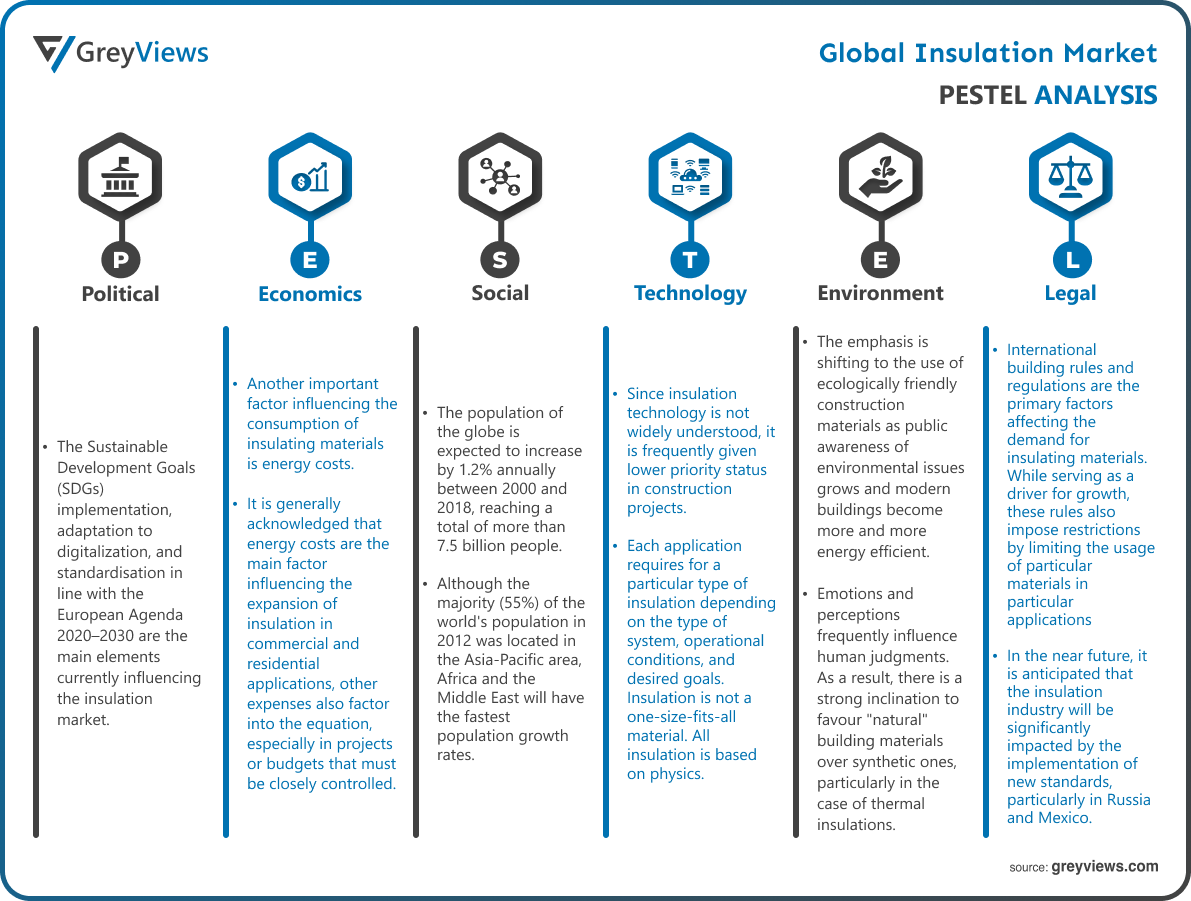

Political Factors- The Sustainable Development Goals (SDGs) implementation, adaptation to digitalization, and standardisation in line with the European Agenda 2020–2030 are the main elements currently influencing the insulation market. Respondents in the participant countries highlighted two opposing points of view: some respondents emphasised the need for the insulation products to be competitive on its own, while others emphasised the crucial role of the public sector as a propeller for development.

Economical Factors- Another important factor influencing the consumption of insulating materials is energy costs. Although it is generally acknowledged that energy costs are the main factor influencing the expansion of insulation in commercial and residential applications, other expenses also factor into the equation, especially in projects or budgets that must be closely controlled. This is also true of production expenses, where energy frequently makes up a significant component, particularly in the glass and mineral wool market, which takes a lot of energy in furnaces and ovens.

In this regard, developing shale gas as a feedstock for numerous monomers and polymers is considered a key opportunity for the insulation market as it will aid in containing manufacturing costs and could present new projects.

Social Factors- The population of the globe is expected to increase by 1.2% annually between 2000 and 2018, reaching a total of more than 7.5 billion people. Although the majority (55%) of the world's population in 2012 was located in the Asia-Pacific area, Africa and the Middle East will have the fastest population growth rates. The fact that the world's population is expanding and relocating from rural areas to urban centres, which increases demand for both commercial and residential buildings as well as the related infrastructure and services, is most significant in terms of sustainable insulation.

Technological Factors- Since insulation technology is not widely understood, it is frequently given lower priority status in construction projects. Each application requires for a particular type of insulation depending on the type of system, operational conditions, and desired goals. Insulation is not a one-size-fits-all material. All insulation is based on physics. The key scientific fields in insulation include thermal dynamics, heat transfer/flow, fluid dynamics, wave theory, and acoustical dynamics. Insulation can lessen acoustic energy transmission as well as energy transfer in the form of heat flow.

Environmental Factors- The emphasis is shifting to the use of ecologically friendly construction materials as public awareness of environmental issues grows and modern buildings become more and more energy efficient. Emotions and perceptions frequently influence human judgments. As a result, there is a strong inclination to favour "natural" building materials over synthetic ones, particularly in the case of thermal insulations. By providing researchers and building designers with an impartial decision-making tool to assess the environmental impact of building products, building components, and buildings as a whole, life cycle assessment (LCA) has provided an opportunity to broaden the meaning of the term "environmentally friendly."

Legal Factors- International building rules and regulations are the primary factors affecting the demand for insulating materials. While serving as a driver for growth, these rules also impose restrictions by limiting the usage of particular materials in particular applications. In the near future, it is anticipated that the insulation industry will be significantly impacted by the implementation of new standards, particularly in Russia and Mexico. Quantifying this impact, however, is challenging and extremely speculative.

- Introduction

- 1. Objectives of the Study

- 2. Market Definition

- 3. Research Scope

- Research Methodology and Assumptions

- Executive Summary

- Premium Insights

- 1. Porter’s Five Forces Analysis

- 2. Value Chain Analysis

- 3. Top Investment Pockets

- 3.1. Market Attractiveness Analysis By Product

- 3.2. Market Attractiveness Analysis By End-Use

- 3.3. Market Attractiveness Analysis By Region

- 4. Industry Trends

- Market Dynamics

- 1. Market Evaluation

- 2. Drivers

- 2.1. Residential Sector is Rising

- 3. Restraints

- 3.1. Environmental Concerns

- 4. Opportunities

- 4.1. Increase in the Government Policies

- 5. Challenges

- 5.1. Fluctuating Raw Material Prices

- Global Insulation Market Analysis and Projection, By Product

- 1. Segment Overview

- 2. Glass Wool

- 3. EPS

- 4. XPS

- 5. Mineral Wool

- 6. CMS Fibre

- 7. Calcium Silicate

- 8. Aerogel

- 9. Cellulose

- PIR

- Phenolic Foam

- Polyurethane

- Global Insulation Market Analysis and Projection, By End-Use

- 1. Segment Overview

- 2. Construction

- 3. Industrial

- 4. Transportation

- 5. HVAC & OEM

- 6. Appliances

- 7. Furniture/Bedding

- 8. Packing

- Global Insulation Market Analysis and Projection, By Regional Analysis

- 1. Segment Overview

- 2. North America

- 2.1. U.S.

- 2.2. Canada

- 2.3. Mexico

- 3. Europe

- 3.1. Germany

- 3.2. France

- 3.3. U.K.

- 3.4. Italy

- 3.5. Spain

- 4. Asia-Pacific

- 4.1. Japan

- 4.2. China

- 4.3. India

- 5. South America

- 5.1. Brazil

- 6. Middle East and Africa

- 6.1. UAE

- 6.2. South Africa

- Global Insulation Market-Competitive Landscape

- 1. Overview

- 2. Market Share of Key Players in the Insulation Market

- 2.1. Global Company Market Share

- 2.2. North America Company Market Share

- 2.3. Europe Company Market Share

- 2.4. APAC Company Market Share

- 3. Competitive Situations and Trends

- 3.1. Product Launches and Developments

- 3.2. Partnerships, Collaborations, and Agreements

- 3.3. Mergers & Acquisitions

- 3.4. Expansions

- Company Profiles

- GAF Materials Corp.

- 1.1. Business Overview

- 1.2. Company Snapshot

- 1.3. Company Market Share Analysis

- 1.4. Company Product Portfolio

- 1.5. Recent Developments

- 1.6. SWOT Analysis

- Huntsman International LLC

- 2.1. Business Overview

- 2.2. Company Snapshot

- 2.3. Company Market Share Analysis

- 2.4. Company Product Portfolio

- 2.5. Recent Developments

- 2.6. SWOT Analysis

- Johns Manville

- 3.1. Business Overview

- 3.2. Company Snapshot

- 3.3. Company Market Share Analysis

- 3.4. Company Product Portfolio

- 3.5. Recent Developments

- 3.6. SWOT Analysis

- Cellofoam North America, Inc.

- 4.1. Business Overview

- 4.2. Company Snapshot

- 4.3. Company Market Share Analysis

- 4.4. Company Product Portfolio

- 4.5. Recent Developments

- 4.6. SWOT Analysis

- Rockwool International A/S

- 5.1. Business Overview

- 5.2. Company Snapshot

- 5.3. Company Market Share Analysis

- 5.4. Company Product Portfolio

- 5.5. Recent Developments

- 5.6. SWOT Analysis

- DuPont

- 6.1. Business Overview

- 6.2. Company Snapshot

- 6.3. Company Market Share Analysis

- 6.4. Company Product Portfolio

- 6.5. Recent Developments

- 6.6. SWOT Analysis

- Owens Corning

- 7.1. Business Overview

- 7.2. Company Snapshot

- 7.3. Company Market Share Analysis

- 7.4. Company Product Portfolio

- 7.5. Recent Developments

- 7.6. SWOT Analysis

- Atlas Roofing Corp.

- 8.1. Business Overview

- 8.2. Company Snapshot

- 8.3. Company Market Share Analysis

- 8.4. Company Product Portfolio

- 8.5. Recent Developments

- 8.6. SWOT Analysis

- Saint-Gobain S.A.

- 9.1. Business Overview

- 9.2. Company Snapshot

- 9.3. Company Market Share Analysis

- 9.4. Company Product Portfolio

- 9.5. Recent Developments

- 9.6. SWOT Analysis

- Kingspan Group

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Product Portfolio

- Recent Developments

- SWOT Analysis

- GAF Materials Corp.

List of Table

- Global Insulation Market, By Product, 2021–2029 (USD Billion)

- Global Glass Wool, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global EPS, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global XPS, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Mineral Wool, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global CMS Fibre, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Calcium Silicate, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Aerogel, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Cellulose, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global PIR, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Phenolic Foam, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Polyurethane, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Global Construction, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Industrial, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Transportation, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global HVAC & OEM, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Appliances, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Furniture/Bedding, Insulation Market, By Region, 2021–2029 (USD Billion)

- Global Packing, Insulation Market, By Region, 2021–2029 (USD Billion)

- North America Insulation Market, By Product, 2021–2029 (USD Billion)

- North America Insulation Market, By End-Use, 2021–2029 (USD Billion)

- USA Insulation Market, By Product, 2021–2029 (USD Billion)

- USA Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Canada Insulation Market, By Product, 2021–2029 (USD Billion)

- Canada Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Mexico Insulation Market, By Product, 2021–2029 (USD Billion)

- Mexico Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Europe Insulation Market, By Product, 2021–2029 (USD Billion)

- Europe Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Germany Insulation Market, By Product, 2021–2029 (USD Billion)

- Germany Insulation Market, By End-Use, 2021–2029 (USD Billion)

- France Insulation Market, By Product, 2021–2029 (USD Billion)

- France Insulation Market, By End-Use, 2021–2029 (USD Billion)

- UK Insulation Market, By Product, 2021–2029 (USD Billion)

- UK Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Italy Insulation Market, By Product, 2021–2029 (USD Billion)

- Italy Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Spain Insulation Market, By Product, 2021–2029 (USD Billion)

- Spain Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Asia Pacific Insulation Market, By Product, 2021–2029 (USD Billion)

- Asia Pacific Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Japan Insulation Market, By Product, 2021–2029 (USD Billion)

- Japan Insulation Market, By End-Use, 2021–2029 (USD Billion)

- China Insulation Market, By Product, 2021–2029 (USD Billion)

- China Insulation Market, By End-Use, 2021–2029 (USD Billion)

- India Insulation Market, By Product, 2021–2029 (USD Billion)

- India Insulation Market, By End-Use, 2021–2029 (USD Billion)

- South America Insulation Market, By Product, 2021–2029 (USD Billion)

- South America Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Brazil Insulation Market, By Product, 2021–2029 (USD Billion)

- Brazil Insulation Market, By End-Use, 2021–2029 (USD Billion)

- Middle East and Africa Insulation Market, By Product, 2021–2029 (USD Billion)

- Middle East and Africa Insulation Market, By End-Use, 2021–2029 (USD Billion)

- UAE Insulation Market, By Product, 2021–2029 (USD Billion)

- UAE Insulation Market, By End-Use, 2021–2029 (USD Billion)

- South Africa Insulation Market, By Product, 2021–2029 (USD Billion)

- South Africa Insulation Market, By End-Use, 2021–2029 (USD Billion)

List of Figures

- Global Insulation Market Segmentation

- Insulation Market: Research Methodology

- Market Size Estimation Methodology: Bottom-Up Approach

- Market Size Estimation Methodology: Top-Down Approach

- Data Triangulation

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Global Insulation Market Attractiveness Analysis By Product

- Global Insulation Market Attractiveness Analysis By End-Use

- Global Insulation Market Attractiveness Analysis By Region

- Global Insulation Market: Dynamics

- Global Insulation Market Share By Product (2021 & 2029)

- Global Insulation Market Share By End-Use (2021 & 2029)

- Global Insulation Market Share by Regions (2021 & 2029)

- Global Insulation Market Share by Company (2020)

Choose License Type

GreyViews is one of the leading providers of market intelligence products and services. We offer reports on over 10+ industries and update our collection daily which helps our clients to access database of expert market insights on global industries, companies, products, and trends.